This share prices have a 15 minute delay and are shown in the local time of the market in which the quote is displayed.

Fintechs are companies that use new technologies to offer banking services. How can they help us with our finances?

The word fintech, which combines “finance” and “technology”, conceptually refers to companies that can offer agile and convenient digital services for advice, asset management, personal finance, alternative financing or electronic payments through innovative technologies that give users greater access to banking. How do fintechs do this?

Let's look at an example. Imagine a financial startup created in a small office in downtown Santiago, Chile to offer quick online loans, investment advice, financial product comparisons and other services. What novelty does it offer? Its capacity to offer all these services online through new technological tools like blockchain. What makes this technology so significant? Find out on the Banco Santander Spain blog or check out this article on blockchain from the Finanzas para Mortales (‘Finance for Mortals’) website.

What types of fintech are there?

We can find various types of fintechs. Some are merely electronic payment platforms or only offer international transfers, while others may focus on online credit products, accounting software and billing systems, personal finance management, robo-advisory service, insurance, blockchain solutions, and digital securities brokerage services, or allow users to order funds or invest.

In addition to the many services they offer, fintechs can also operate in a broad network of markets and for a broad range of customers. Hence they are intended for individuals, for-profit companies, institutions, etc.

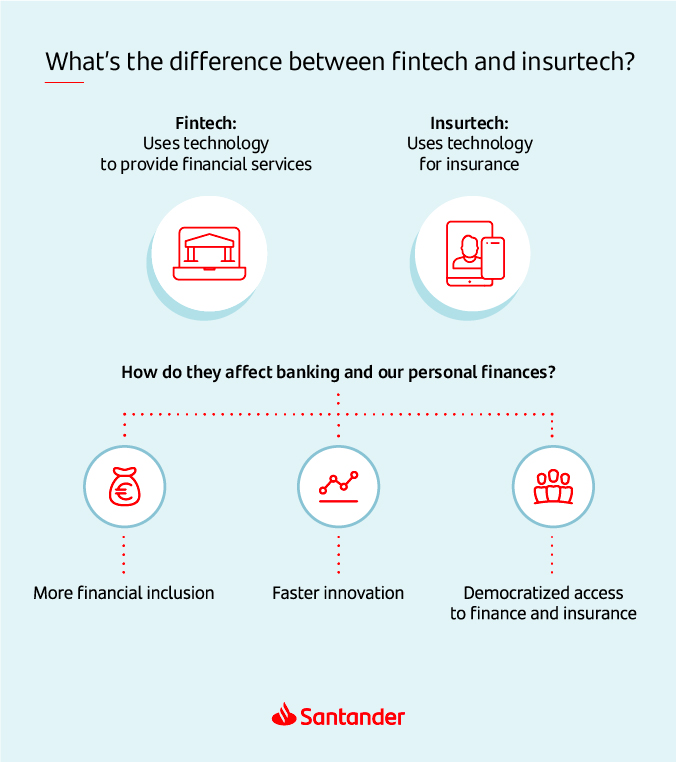

What’s the difference between an insurtech and a fintech?

The terms fintech and insurtech often appear together but are not the same. This Santander Brazil article teaches you what an insurtech is. To find out the main differences between a fintech and an insurtech, look at this infographic.

What can fintechs do for our personal finances?

As users, we can turn to fintechs for such services as money or investment management, financial product comparisons, loan applications or advice.

Fintech services are easy to use and help us manage our personal finance simply and securely.

Fintechs have a flexible structure and agile methods for all segments. Their entry into the market opens up many benefits of traditional financial institutions to unbanked customers but without brokerage fees and at lower costs. That relationship helps increase financial inclusion, as noted by the Institute of International Finance, with significant stories of success at Santander involving our support for fintechs like ePesos and PayJoy.

What should we consider when using a fintech?

The outburst of banking technology has major new advantages, like making financial services simpler and more affordable. However, like any activity, it carries risks that we need to think about. In particular, users should take into account these aspects when resorting to a fintech:

- Get confirmation that the fintech will protect your data and understand what it will do with them.

- Always aware about what services you’re signing up for.

- Check that the company complies with all legal requirements and is authorized to provide the service you seek.

- Fintechs run the risk of using technology still in its early stages, even if it’s deemed highly successful and efficient.

Nevertheless, fintechs appeared on the banking scene some time ago, able to reach many market segments and promote financial inclusion, with support from authorities. They can also significantly boost digitalization around the world.

How are fintechs different to traditional banks?

While fintechs generally sell customers a single service or product using innovative technology, traditional banks are more focused on solving general user problems and making sales that involve more products. Still, the differences between them have narrowed quickly in recent years. Traditional banks have also jumped on the digital bandwagon with new models and solutions whose main ingredients are cutting-edge technology and innovation, as noted in this article on Finanzas para Mortales (“Finance for Mortals”).

Still, banks are demanding that both fintechs and traditional banks be subject to the same regulations, according to the Institute of International Finance. This Finanzas para Mortales article explains the need for a common framework so the two play by the same rules.

Overall, fintechs have proved to provide major opportunities for partnerships with banks to offer customers new products, like the case of Santander Mexico’s Radar programme. It aims to find high-potential technology start-ups for alliances with Santander Mexico to improve services and, in particular, promote financial inclusion. Read this article to find out more about "Radar".