Household budgets go hand in hand with saving. Making a list of income and expenses in a fixed period can help households be more financially sound. Below we tell you how to draw up a budget that reflects your financial situation and needs.

What is a budget?

A calculation of the money needed to cover prior known expenses. It’s the amount we need to achieve a goal like refurbishing the kitchen, getting married, renting a home, buying a motorbike, changing car or making our savings target.

A case study: Marina and her family want to move to a bigger apartment, but she’s not sure they can afford it. If they do take the plunge, she needs to know what house size and which neighbourhoods fit into her price range. Essentially, what's María’s budget for moving house?

Marina grabs a calculator and gets to work. She makes a list of her income and expenses, including all move-related costs: removal service, refurbishments, cleaning, new furniture, home insurance, selling her current home... Now she knows how much money she has to start looking for somewhere new.

Drawing up a budget means planning every income and expense over a set period. The outcome is a limit to what we can spend each month to make sure we achieve our goal, which isn’t always necessarily a purchase. Household budgets often serve as a means of knowing how much we’re able to save. By planning ahead like Marina’s family, we can have a better idea of how far our money will go. To learn more, read this post by Finanzas para Mortales (Finance for Mortals).

How to draw up a household budget in six steps

Now we know how useful they are, let's look at what you need to do to come up with the best possible budget:

- First, gather every piece of information on the household’s finances, like bank statements, payslips, purchase receipts, fixed costs and debts. That means every income and expense, with no exceptions.

- Record them in an Excel spreadsheet or whatever tool you’re planning to use (like an app). Whatever the format, the next step is to break down each item so they are orderly, clear and easy-to-find.

- In the same document or tool, detail each movement performed in a month. To help you organize, you could use these categories: income (such as salary and benefits), fixed costs (like water and electricity), essential variable costs (repairs) and unnecessary or “ant” expenses (pay TV or eating out).

- Now it's time to think about savings. Include a section on how much of your income you want to put away each month.

- Now that you’ve categorized your budget, work out the difference between your income and expenses to determine your household's financial balance. Any spare money is how much you’re able to save. If the result is negative, take a close look at the budget and think about why you’re spending more money than you’re bringing in.

- Now’s the time to make adjustments so you can reach the amount you want to save. You may want to increase or decrease it according to your circumstances or needs.

Placing the items in categories will give a full picture of your finances and money management. You’ll also be able to see your unnecessary spending and things to cut down on if you want to (or can); whether you want to boost your savings; if you have money to invest in financial instruments; if you’re paying the best prices; and if you’re managing your money properly.

You should also set aside time to scrutinize how much you spend and on what. That way, you can cap your expenses and estimate how much you can really save. You can only do that by sticking to your budget.

Ideal household budget: tips

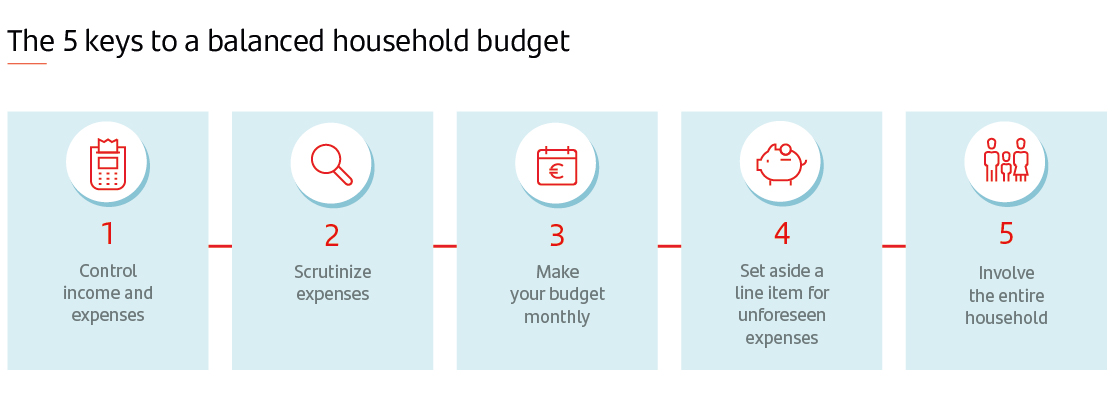

There is no one-size-fits-all way to budget because each household is different. However, we can give tips on how to be financially healthy:

- Involving every household member can unearth new ideas and make sure everyone sticks to the budget.

- Controlling every expense makes it easier to reach financial goals.

- Setting aside a line item for unforeseen expenses can give a little more leeway.

- Although the budget is monthly, it’s important to review it regularly to see whether any items have changed.

- To make sure you save, include the “savings” category as a fixed cost.

Household budgets: how they can help

Drawing up a household budget lets us know how far our income will stretch so we can take greater control of our family finances. It’s important to strike a balance. We can adjust each expense and need to our priorities. This can also help stave off debt and give a better view of the future as we’ll be able to save more, have a safety net against unpleasant surprises, and tweak each item if our circumstances change.