Shareholders and investors need to understand financial concepts about listed companies. One that really interests them is the “payout”: the share of profits that a company “pays out” to them. Below is everything you need to know about payouts.

A payout is the share of profits that a listed company will pay its shareholders. If the payout set out in the company’s shareholder remuneration policy is 50%, the company will distribute half of its net profits among its shareholders.

If that policy says the 50% payout should be split between a cash dividend and share buybacks, the formula is:

Payout = (cash dividend + share buyback)/underlying net profit. The payout is expressed as a percentage.

Remember, a dividend is cash paid to shareholders for their share in the company's profits. A share buyback and the subsequent cancellation of shares are when the company “buys back” its own shares to reduce outstanding share capital and increase its share price.

Why do payouts matter to shareholders?

The payout is an indicator that influences an investor’s decision to buy shares in a company. It shows what share of the company’s profits will be paid to shareholders, whether in a cash dividend, a share buyback or both.

What does this mean?

A payout policy can also help attract more long-term investment in a listed company. But the company must find the right balance between shareholder returns and reinvesting in its own long-term growth. A payout gives substance to shareholder remuneration policies, which influence investors’ decisions.

Santander’s payout

The 2026 general shareholders’ meeting approved a final cash dividend of €12.50 cents per share against H2 2025 results, which was paid in May 2026.

Considering the interim cash dividend of €11.50 cents per share paid in November 2025, the total cash dividend per share paid against 2025 results was €24.00 cents, 14% higher than that paid against 2024 results.

On 3 February 2026, the board of directors approved the Second 2025 Buyback Programme worth up to €5,030 million. The programme started on 4 February 2026.

This programme includes €1,830 million as part of our ordinary shareholder remuneration policy charged against H2 2025 results and the remaining amount corresponds to an extraordinary buyback of €3,200 million, equivalent to approximately 50% of the CET1 capital generated following completion of the Poland disposal.

This programme puts us on track to achieve our goal of distributing at least €10 billion through share buybacks charged against 2025 and 2026 results and against expected capital excess1. Considering the share buyback currently underway, we have already carried out approximately 80% of this goal.

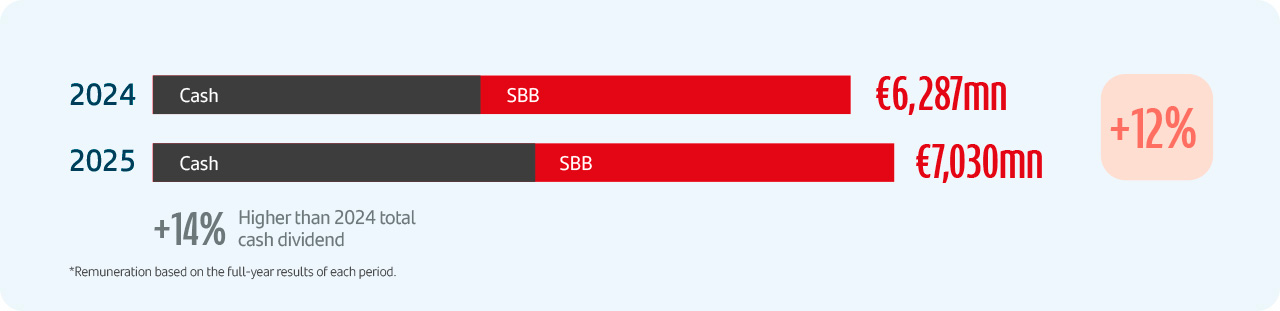

Considering the cash dividends and the two share buybacks as part of our ordinary payout policy, total shareholder remuneration charged against 2025 results will be around €7,030 million (approximately 50% of the Group’s 2025 net reported profit, excluding non-cash, non-capital ratios impact items), split almost evenly between cash dividends and share buybacks. This is a 12% increase compared to the ordinary shareholder remuneration charged against 2024 results.

1. As previously announced, Santander intends to allocate at least €10 billion to shareholders through share buybacks charged against 2025 and 2026 results and against the expected capital excess. This share buyback target includes: i) buybacks that are part of the existing shareholder remuneration policy; and ii) additional buybacks following the publication of annual results to distribute year-end excesses of CET1 capital. The implementation of the shareholder remuneration policy and additional buybacks is subject to corporate and regulatory decisions and approvals.