Listed companies reward their shareholders with a portion of their profits. Cash dividends are the most common form of this reward. But some companies' shareholder remuneration offers up an alternative: the share buyback. Here we tell you about our shareholder remuneration.

The 2026 general shareholders’ meeting approved a final cash dividend of €12.50 cents per share against H2 2025 results, which was paid in May 2026.

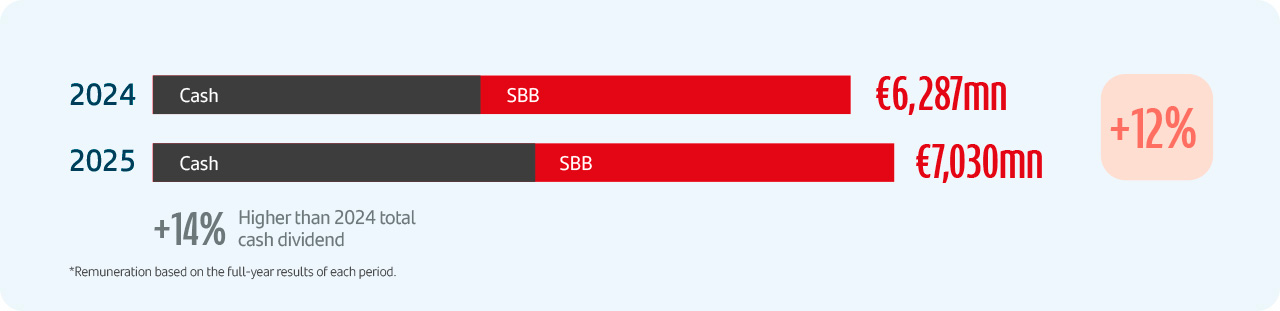

Considering the interim cash dividend of €11.50 cents per share paid in November 2025, the total cash dividend per share paid against 2025 results was €24.00 cents, 14% higher than that paid against 2024 results.

On 3 February 2026, the board of directors approved the Second 2025 Buyback Programme worth up to €5,030 million. The programme started on 4 February 2026.

This programme includes €1,830 million as part of our ordinary shareholder remuneration policy charged against H2 2025 results and the remaining amount corresponds to an extraordinary buyback of €3,200 million, equivalent to approximately 50% of the CET1 capital generated following completion of the Poland disposal.

This programme puts us on track to achieve our goal of distributing at least €10 billion through share buybacks charged against 2025 and 2026 results and against expected capital excess1. Considering the share buyback currently underway, we have already carried out approximately 80% of this goal.

Considering the cash dividends and the two share buybacks as part of our ordinary payout policy, total shareholder remuneration charged against 2025 results will be around €7,030 million (approximately 50% of the Group’s 2025 net reported profit, excluding non-cash, non-capital ratios impact items), split almost evenly between cash dividends and share buybacks. This is a 12% increase compared to the ordinary shareholder remuneration charged against 2024 results.

1. As previously announced, Santander intends to allocate at least €10 billion to shareholders through share buybacks charged against 2025 and 2026 results and against the expected capital excess. This share buyback target includes: i) buybacks that are part of the existing shareholder remuneration policy; and ii) additional buybacks following the publication of annual results to distribute year-end excesses of CET1 capital. The implementation of the shareholder remuneration policy and additional buybacks is subject to corporate and regulatory decisions and approvals.

As a result of our strong capital generation, we expect to reward shareholders with 10 billion euros in share buy-backs for 2025 and 2026 and with excess capital, in addition to the ordinary distribution of cash dividends.

What is a share buyback programme and why is it important for shareholders?

Share buyback is a form of remuneration for a company's shareholders. A share buyback is when companies buy back their own shares from the market, cancel them and, ultimately, reduce share capital. With fewer shares in circulation, each shareholder gets both a larger stake in the company and a higher return on future dividends.

What are the benefits of a share buyback

Here are some of the ways that buybacks work to shareholders' advantage under normal market conditions:

- First, since the company’s value remains the same but the supply of shares is lower, the share price will increase. However, that depends on market behaviour.

- Second, the earnings per share (EPS) should increase because fewer shares are in circulation. Shareholders will have a greater stake in the company’s profits.

- Unless a shareholder chooses to offload their shares, a buyback is a tax-free transaction.

Imagine a listed company with 1,000 shares, and 100 (10%) of them are held by one shareholder. The company runs a share buyback programme and purchases 100 shares, reducing total share capital to 900 shares. The shareholder, whose stake has just increased by 1.11% to 11.11%, is now entitled to more of the company's profits. Also, the share price should become more attractive to investors.

In short, a share buy-back programme allows companies to generate additional value for their shareholders. Under normal market conditions, the portion of profits that listed companies use to buy back their own shares directly benefits the price of the shares.