A type of financial asset, the technology underpinned by a technology with great potential, that increases security, traceability and transparency in data networks and systems.

Digitalisation has become increasingly important in many aspects of our lives. It has also is having an impact on money. It is important to differentiate digital money from electronic money which we trade with today in our day-to-day or see in our bank account. The latter is possible all thanks to the brokering of financial agents who cover credit risks. Digital money would ideally preserve the characteristics of cash (instant liquidation, it belongs to the holder, and no need for intermediaries in the exchange).

Recent decades have seen various attempts to create digital money, but they have all failed for one reason or another - or didn't garner the necessary traction. The most active groups of people in this innovation have been cypherpunks (online groups that value the ability to be anonymous online above all else) and neoliberal economists.

Building on these foundations, Satoshi Nakamoto (whose real identity remains unknown) published, in 2008, an article titled “Bitcoin: a peer-to-peer electronic cash system” in 2008 in which he presented both Bitcoin and the technology underpinning this cryptocurrency: blockchain. All transactions made in Bitcoin are recorded in a proprietary, public blockchain, giving Bitcoin the characteristics of blockchain: irreversibility, distribution and security.

What's more, Bitcoin seeks to be a decentralised means of payment, which means that no central body (e.g., a central bank) decides on its issuance or ensures how secure its transactions are. The algorithm governing Bitcoin dictates that a set number of bitcoins are issued every time a block of information joins its blockchain (this will be miners' remuneration), with this number decreasing over time.

When the first bitcoin transaction took place in 2009 and the first block of information was mined, 50 bitcoins were issued, although this number was halved when the network reached 200,000 blocks. It’s expected to continue to decrease, successively it will be halved, approximately every 4 years, until the expected 21 million bitcoins are issued in 2140. Due to the rigidity of Bitcoin protocol's monetary policy and its decentralisation, one of the most central narratives behind the cryptoasset is that it is “digital gold”.

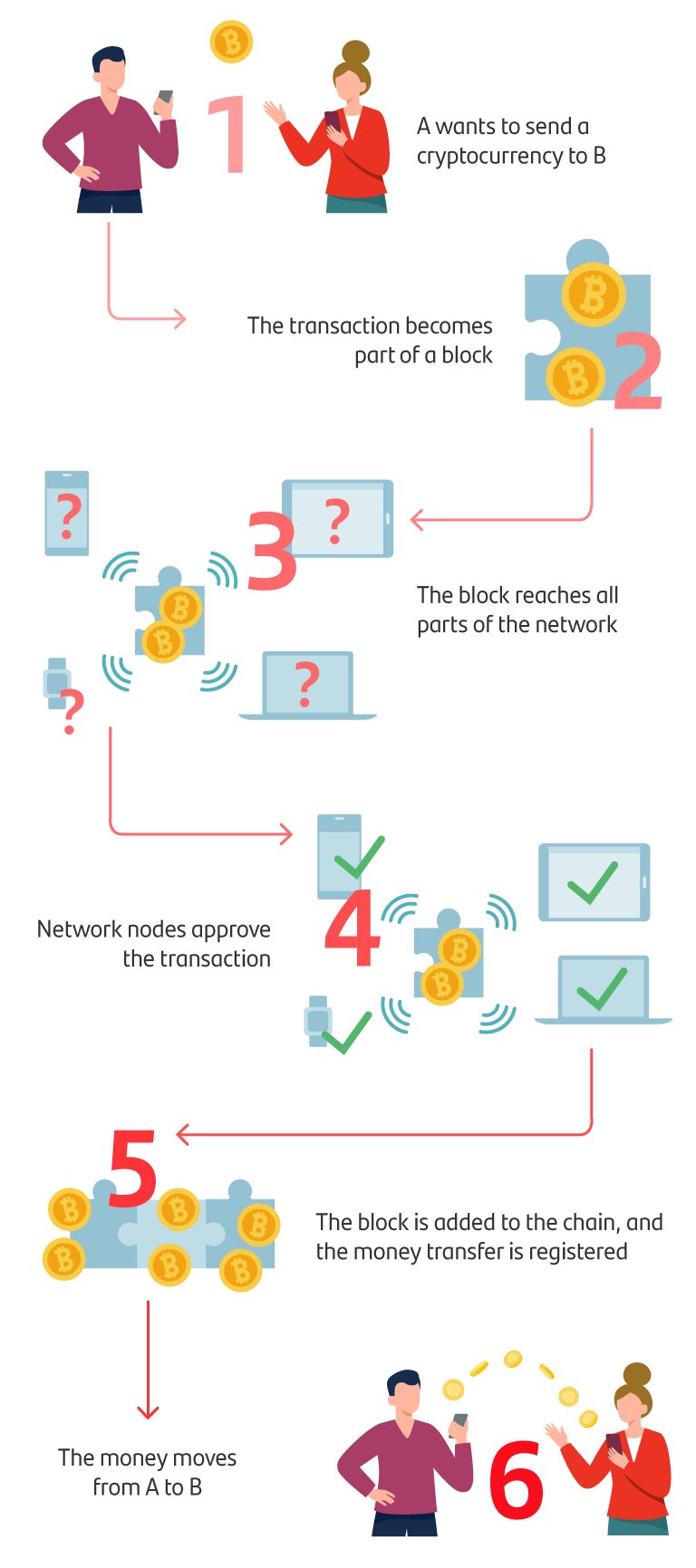

Bitcoin transactions work as follows: If A wants to send a bitcoin to B, A must convey this request to the system in an action similar to the way traditional bank transfers are sent. Once the network receives this order, it then goes on to form part of a block (a block of information, as mentioned earlier). The network will confirm the signature of the transaction (this means that A has really ordered this transaction using his Private Key A) and that A possesses the bitcoin they want to send to B. Once the nodes verify this information, the block of information is added to the chain, the transfer is recorded, and the money moves from one account to the other.

The challenges of Bitcoin

Bitcoin, like other cryptocurrencies, is not entirely risk-free. You can read more in the article “Bitcoins and other cryptocurrencies: everything you need to know”.

This article is for educational purposes only and does not reflect the opinion or strategy of Banco Santander, and in no way should be considered as financial advice.

Note: Cryptoassets are exposed to high risk of illiquidity and full loss, or temporary unavailability of the capital invested, as they are highly speculative products that see highly volatile prices and huge fluctuations in value. Cryptoassets are unregulated and may not be suitable for retail investors. Their prices are set in the absence of mechanisms to ensure their correct formulation, such as those that exist on regulated stock markets. On a similar note, their high dependence on technology can give rise to operational faults, cyberthreats and risks arising from holding cryptoassets under the applicable legal framework, and credentials or passwords can be stolen or lost. Cryptoassets also entail the risk of fraud or money laundering. This means that cryptoassets may not fall under EU regulations and would therefore be unprotected, meaning that the capital invested may not be covered by the Deposit Guarantee Fund or the Investment Guarantee Fund. Any potential issues may, therefore, be rather costly to resolve.